Updated October 9, 2021

A trust is a legal way to set aside assets for a specific purpose. A living trust is one that is initiated while you are still alive, offering flexibility and control over your estates in the event of incapacitation or death. Below are some of the benefits of creating a living trust.

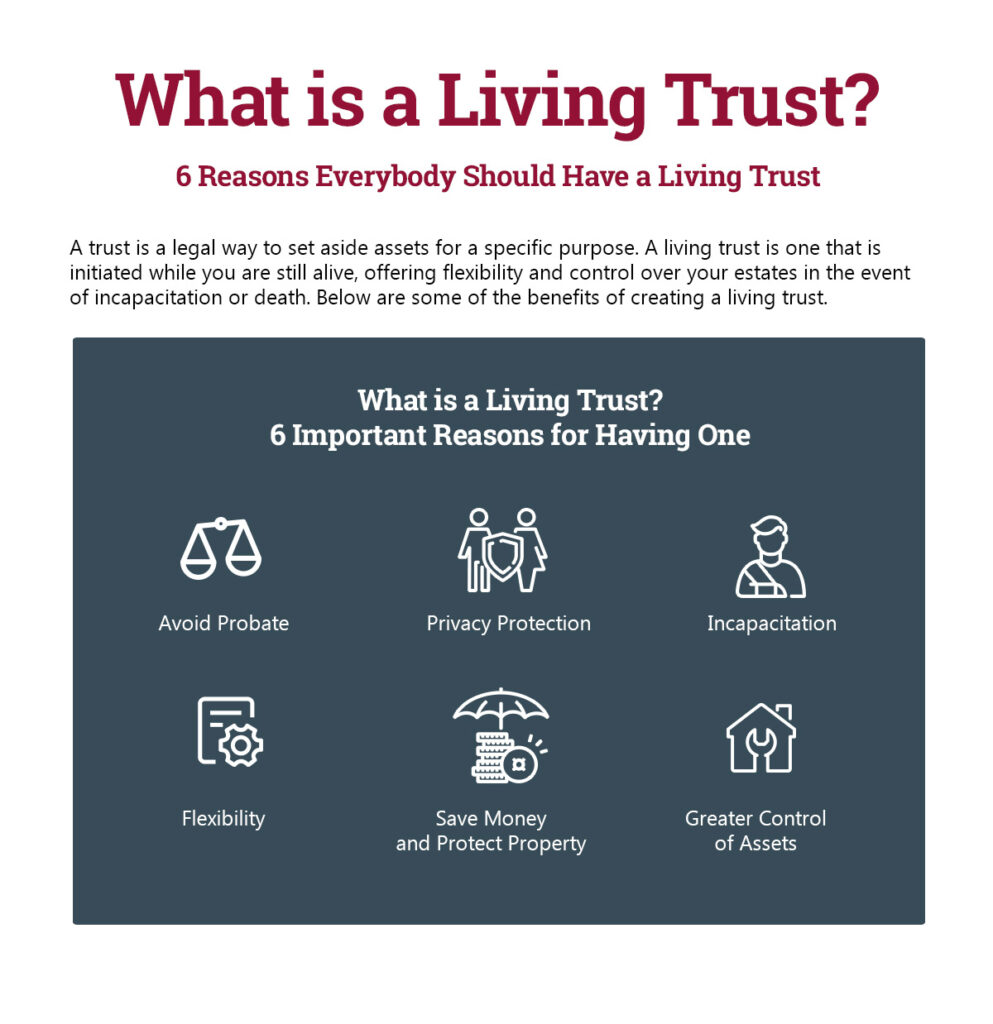

What is a Living Trust? 6 Important Reasons for Having One

- Avoid Probate

- Privacy Protection

- Incapacitation

- Flexibility

- Save Money and Protect Property

- Greater Control of Assets

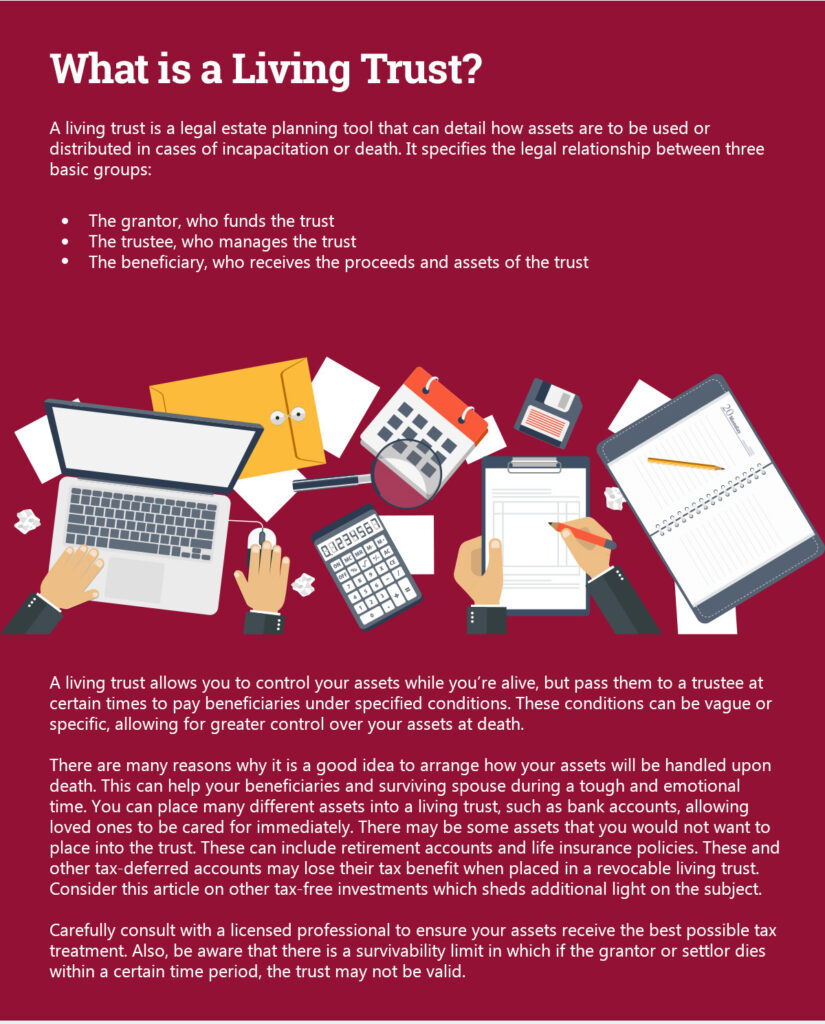

What is a Living Trust?

A living trust is a legal estate planning tool that can detail how assets are to be used or distributed in cases of incapacitation or death. It specifies the legal relationship between three basic groups:

- The grantor, who funds the trust

- The trustee, who manages the trust

- The beneficiary, who receives the proceeds and assets of the trust

A living trust allows you to control your assets while you’re alive, but pass them to a trustee at certain times to pay beneficiaries under specified conditions. These conditions can be vague or specific, allowing for greater control over your assets at death.

“Years ago it was common to talk about a Trust as though Trusts were intended only for extremely wealthy people. We have learned that the need for Trusts has always been there and that the people who should use trusts ought to include people whose estates are relatively small.” – Hugo Melvoin, Tax Attorney, Federal Estate and Gift Taxes Public Hearings (1976)

There are many reasons why it is a good idea to arrange how your assets will be handled upon death. This can help your beneficiaries and surviving spouse during a tough and emotional time. You can place many different assets into a living trust, such as bank accounts, allowing loved ones to be cared for immediately. There may be some assets that you would not want to place into the trust. These can include retirement accounts and life insurance policies. These and other tax-deferred accounts may lose their tax benefit when placed in a revocable living trust. Consider this article on other tax-free investments which sheds additional light on the subject.

Carefully consult with a licensed professional to ensure your assets receive the best possible tax treatment. Also, be aware that there is a survivability limit in which if the grantor or settlor dies within a certain time period, the trust may not be valid.

Revocable vs Irrevocable Trust

A revocable trust is one where the grantor retains the rights to manage the assets and thus can remove assets from the trust. In contrast, an irrevocable trust is one where the grantor relinquishes all rights to the asset. There are some benefits to doing this, usually as a way to avoid certain taxes at death or to remove assets that may otherwise have been used for Medicare proceedings. Trusts can also be set up to pass funds to charities over time which also carries tax benefits. It is also important to consider the living trust cost since it may not be the best option for you.

While there is a higher fee to set up a trust, and you must fund the trust by adding your assets, it can save money and time in the long run. A living trust has many additional benefits as well. Let’s take a closer look at the top 6 reasons for creating a living trust.

Avoid Probate

Probate is the court-led process that usually handles an estate after death and varies based on location. In general, the process involves a court examining the provisions of a will and the assets included (or excluded) in it. Probate also involves attorneys’ fees, as well as court fees and other costs, which can be calculated as a percentage of a total estate. This is one of the main reasons to avoid probate, as the money is deducted from the estate and thus limits what is passed on to your beneficiaries.

There is usually a waiting period from one to three months in which the beneficiaries have limited to no access to any of the funds in the estate while in probate. However, the bills must still be paid. Allowing access to bank accounts or other assets in the trust will allow the surviving spouse or other beneficiaries to access fund needed to pay bills, funeral expenses, taxes and more. A living trust is an effective method of avoiding probate court. Improper planning can leave beneficiaries and a surviving spouse with no funds for a period of time.

Privacy Protection

A will and all assets not covered by a will are subject to probate and thus become open record. The probate process is a matter of public record, which means anyone can look up what assets were in the estate and what beneficiaries received what assets. Some states even allow online access to these records. Setting up a trust is a method of avoiding probate and can also be used to protect the privacy of your estate and thus your beneficiaries. This is especially useful when knowledge of the estate might allow others to try and take advantage of your beneficiaries.

Incapacitation

Another key benefit of living trusts is that they can be enacted when the grantor is incapacitated. The trustee will take control of your assets during this unfortunate situation. The trustee will then manage your estate according to your predefined stipulations, including ensuring the trust is run for your benefit as the trustor. This is different from a power of attorney or health care power of attorney in that it details how your assets are to be managed while you are incapacitated, as well as what to do in the case of your death. Living trusts can also be set up for married couples that will set aside funds or assets to provide for the surviving spouse.

Flexibility

Trusts offer greater flexibility in determining how assets are to be distributed in various situations, including death. A living trust can also detail how assets are to be managed in case you are incapacitated. There are a variety of trusts, such as living trusts, which can be revocable or irrevocable. A revocable living trust can be changed while an irrevocable one may not. There are also a range of other trust options, including as an income-only living trust. It may be a good idea to consult an estate-planning attorney for complex situations to ensure your assets are managed in the best possible way. Living trusts will provide greater flexibility to manage your assets in the way you want, including how they are passed on to heirs.

Save Money and Protect Property

Protecting assets from lawsuits or creditors is a concern when estate planning. Estate taxes and other forms of taxation are also a concern. At death, probate courts can also cut into the value of an estate. There may also be times when an heir is subject to creditors, but you would like to set aside assets for them that cannot be used to satisfy their debts. Certain trusts can be used to set aside assets and real property in a way that protects them from lawyers and creditors. Typically, this involves giving up some form of control over the assets, such as with an irrevocable trust.

There may also be additional tax benefits to consider, such as the possibility of exceeding the high estate tax exemption. This is why a revocable living trust and irrevocable living trust may be important estate planning tools. Certain trusts may even be arranged to be managed overseas to avoid jurisdiction of some courts. Also, trusts can provide benefits in cases of joint tenancy. Since a trust allows for the assets to be split up as desired, it can be parceled out in amounts or in ways that limit the impact of costs while maximizing associated tax benefits. It is important to consult a legal professional before funding any trust to ensure your assets are managed legally.

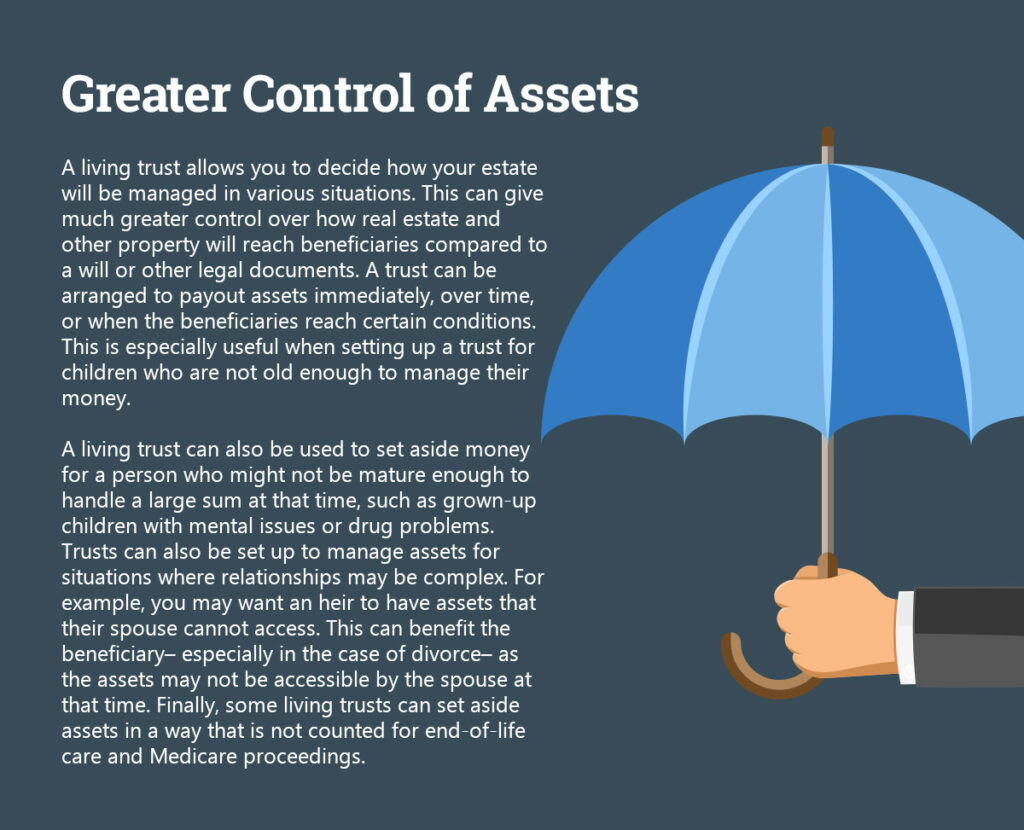

Greater Control of Assets

A living trust allows you to decide how your estate will be managed in various situations. This can give much greater control over how real estate and other property will reach beneficiaries compared to a will or other legal documents. A trust can be arranged to payout assets immediately, over time, or when the beneficiaries reach certain conditions. This is especially useful when setting up a trust for children who are not old enough to manage their money.

A living trust can also be used to set aside money for a person who might not be mature enough to handle a large sum at that time, such as grown-up children with mental issues or drug problems. Trusts can also be set up to manage assets for situations where relationships may be complex. For example, you may want an heir to have assets that their spouse cannot access. This can benefit the beneficiary– especially in the case of divorce– as the assets may not be accessible by the spouse at that time. Finally, some living trusts can set aside assets in a way that is not counted for end-of-life care and Medicare proceedings.

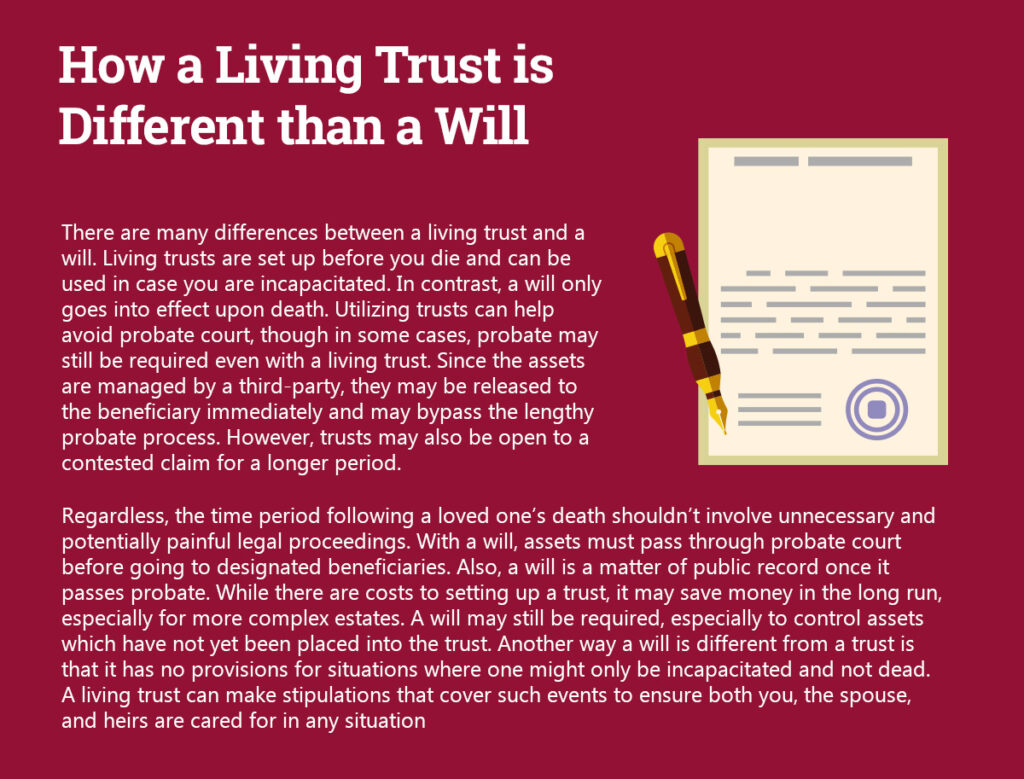

How a Living Trust is Different than a Will

There are many differences between a living trust and a will. Living trusts are set up before you die and can be used in case you are incapacitated. In contrast, a will only goes into effect upon death. Utilizing trusts can help avoid probate court, though in some cases, probate may still be required even with a living trust. Since the assets are managed by a third-party, they may be released to the beneficiary immediately and may bypass the lengthy probate process. However, trusts may also be open to a contested claim for a longer period.

Regardless, the time period following a loved one’s death shouldn’t involve unnecessary and potentially painful legal proceedings. With a will, assets must pass through probate court before going to designated beneficiaries. Also, a will is a matter of public record once it passes probate. While there are costs to setting up a trust, it may save money in the long run, especially for more complex estates. A will may still be required, especially to control assets which have not yet been placed into the trust. Another way a will is different from a trust is that it has no provisions for situations where one might only be incapacitated and not dead. A living trust can make stipulations that cover such events to ensure both you, the spouse, and heirs are cared for in any situation.

What is a Living Trust and How Does it Work?

You may be wondering: What is the purpose of a living revocable trust, and do I need one? The answer depends on your estate and how you would like it to be dispersed after death or if you are incapacitated. It is a powerful legal vehicle that protects assets such as real estate investments, bank accounts, investments, and other real property. How you start your trust depends on where you want to have it, as each state may have different laws regarding trusts and how they are taxed. There are also costs associated with setting up a trust and the time required to fund it.

At death, your wishes will be carried out and passed to your beneficiaries while avoiding the negative aspects of probate court. Since a trust survives the grantor, it can also be used to direct the trustee to manage the assets in certain ways. This can include limiting how the funds are dispersed in certain situations. A living trust can also provide instructions that range from detailed to general in nature. A revocable living trust can be altered and changed when the grantor is alive, while an irrevocable trust is unchangeable. Due to the complex nature of estate planning and tax laws, it is best to consult with a tax professional and attorney to ensure your assets are protected in the most efficient manner.